Private lenders depend on title insurance to protect their security interest in the collateral behind every loan. A standard lender’s title policy provides baseline protection, but experienced originators know that the real strength of a title policy lies in the endorsements attached to it. Endorsements extend coverage to address risks that a base policy simply does not reach, from zoning compliance and survey accuracy to usury protection and environmental liens.

The challenge is that not every endorsement is available in every state, and not every title company is willing to issue the endorsements that are technically available. For private lenders operating across multiple jurisdictions, understanding state-by-state endorsement availability and knowing how to negotiate with reluctant underwriters is a core competency that directly affects portfolio risk.

Why Endorsements Matter More Than Most Lenders Realize

A lender’s title insurance policy without endorsements is a blunt instrument. It confirms that the borrower holds the interest described in the policy and that no undisclosed liens exist as of the policy date. That coverage, while important, leaves significant gaps.

Consider a bridge loan secured by a mixed-use property. Without the right endorsements, the lender may have no coverage for:

- Whether the improvements are actually located within the parcel boundaries

- Whether the property complies with local zoning ordinances

- Whether an existing environmental lien could prime the lender’s deed of trust

- Whether a future court could invalidate the loan on usury grounds

Each of these risks can be addressed through specific ALTA endorsements. ALTA 9 (Restrictions, Encroachments, Minerals) protects against certain covenant violations. ALTA 22 (Location) and ALTA 25 (Same as Survey) confirm the relationship between the survey and the legal description. ALTA 27 (Usury) provides coverage if the loan is later challenged as usurious under applicable law.

Private lenders who skip endorsements because they seem like unnecessary closing costs are making a calculated bet that nothing will go wrong. That bet does not always pay off.

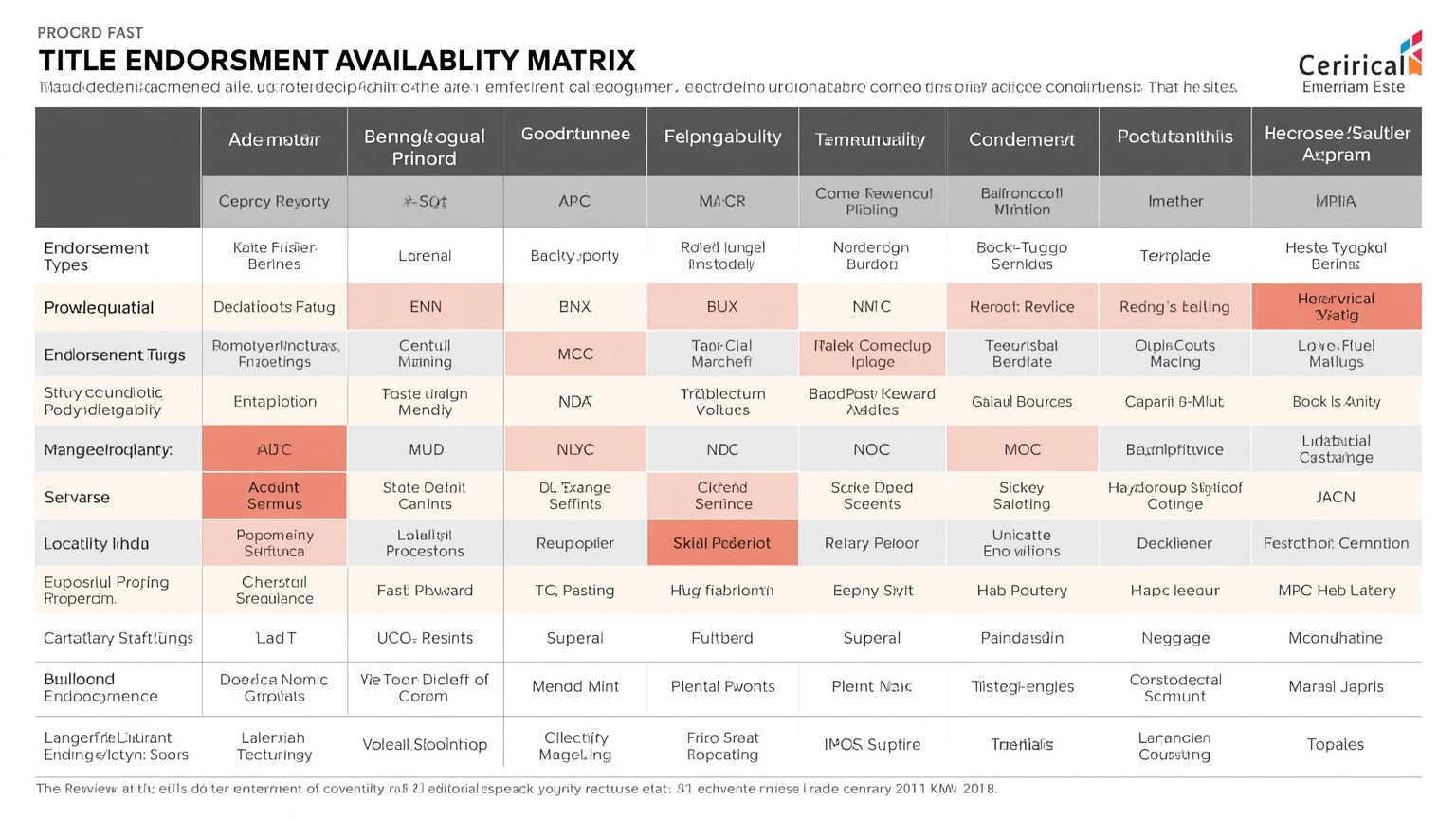

State-by-State Endorsement Availability: The Landscape Private Lenders Must Navigate

Title insurance is regulated at the state level, and that regulation creates a patchwork of endorsement availability that can surprise lenders who originate nationally. Most states adopt the standardized forms published by the American Land Title Association (ALTA), but several important jurisdictions deviate in ways that directly affect private lending transactions.

Texas: A Completely Separate System

Texas is the most distinctive title insurance market in the country. The Texas Department of Insurance prescribes its own policy forms and endorsement schedules, and the state does not use ALTA forms at all. Lenders accustomed to requesting standard ALTA endorsements will find that many of them simply do not exist in their familiar form in Texas.

For example, ALTA 22 (Location), ALTA 25 (Same as Survey), and ALTA 27 (Usury) have no direct Texas equivalents. Some of the coverage these endorsements provide can be obtained through the Texas general endorsement form T-3, but the scope of coverage is not identical. Lenders originating in Texas need to work with title counsel who understands the Texas-specific endorsement framework and can identify where coverage gaps exist relative to what the lender would receive in an ALTA jurisdiction.

The practical impact for private lenders is significant. A lender who closes loans in both California and Texas using the same endorsement checklist will find that checklist only partially applicable in Texas. Loan documents, closing instructions, and internal compliance procedures all need to account for this difference.

Florida: ALTA Forms with State-Specific Modifications

Florida permits the use of ALTA policy forms but requires what the industry calls “Florida Modifications.” These modifications adjust the coverage provided by standard ALTA endorsements, sometimes expanding coverage and sometimes restricting it relative to the unmodified ALTA version.

For private lenders, the key takeaway is that an ALTA endorsement issued in Florida may not provide exactly the same protection as the identical endorsement number issued in Arizona or Oregon. Lenders should review the Florida-modified language with counsel to confirm that the coverage they expect is actually what the endorsement delivers in Florida.

California: Two Endorsement Systems Working in Parallel

California presents private lenders with a unique advantage: two parallel endorsement systems. In addition to the standard ALTA endorsement forms, California title companies also offer endorsements published by the California Land Title Association (CLTA).

This dual system creates flexibility. When a title company declines to issue a particular ALTA endorsement due to underwriting concerns or risk tolerance, the lender can often request a comparable CLTA endorsement that provides similar coverage under a different form number. The CLTA forms are sometimes more readily available because California title companies have deeper familiarity with them and may be more comfortable with the risk profile they represent.

Experienced private lending counsel in California will maintain a cross-reference between ALTA and CLTA endorsement forms so they can quickly identify alternatives when an ALTA endorsement is unavailable for a particular transaction.

Iowa: No Title Insurance at All

Iowa occupies a category entirely its own. It is the only state in the nation that prohibits private title insurance companies from issuing policies. Instead, Iowa uses a system of attorney title opinions and title guaranty certificates issued through the Iowa Title Guaranty Division, a quasi-governmental entity.

For private lenders considering Iowa transactions, this means the entire framework for title protection is different. There are no endorsements to request because there is no title insurance policy to endorse. The protections available through the title guaranty system are different in scope and structure from what a lender would receive through a standard ALTA policy with endorsements. Any lender originating in Iowa needs specialized guidance from counsel familiar with the Iowa title guaranty framework.

When the Title Company Says No: Practical Strategies for Private Lenders

Even in states where a particular endorsement is technically available, title companies sometimes refuse to issue it. This refusal is not always based on regulatory prohibition. More often, it reflects the individual title company’s or underwriter’s assessment of risk on the specific transaction.

Title companies are in the business of managing risk, and their appetite for that risk varies. A large national underwriter may freely issue an endorsement that a regional title company considers too risky on the same property. A title company that issues ALTA 9 endorsements routinely on residential transactions may balk at issuing the same endorsement on a commercial property with complex CC&Rs.

For private lenders, a title company’s refusal to issue a requested endorsement should not be accepted as the final word. There are several strategies that can produce a different result.

Demand a specific explanation for the refusal. Title companies sometimes decline endorsements reflexively or because of internal policies that have not been updated. Asking the underwriter to articulate the specific risk that prevents issuance can sometimes reveal that the concern is manageable or based on incomplete information about the transaction.

Request alternative endorsement forms. This is particularly effective in California, where a CLTA endorsement may provide substantially similar coverage to a declined ALTA form. In other states, there may be modified or limited versions of an endorsement that address the lender’s core concern without requiring the title company to take on the full risk of the standard form.

Ask for removal of the related exception instead. If a title company will not issue an endorsement that would provide affirmative coverage over a particular risk, the lender can ask the company to remove the corresponding exception from Schedule B of the policy. This achieves a similar result through a different mechanism: rather than adding coverage, it removes the exclusion.

Engage a different title company. Risk tolerance varies meaningfully across title companies and underwriters. If one company refuses an endorsement, another may issue it without hesitation. Private lenders who maintain relationships with multiple title companies have leverage that single-source lenders lack. The willingness to move a transaction to a competing title company is often the most effective negotiating tool available.

Building a Systematic Approach to Endorsement Management

Private lenders who originate across multiple states should develop a jurisdiction-specific endorsement matrix that identifies which endorsements are available, which require modified forms, and which are simply unavailable in each state where they lend. This matrix should be reviewed and updated annually as states periodically revise their title insurance regulations.

Equally important is building relationships with title companies and underwriters who understand private lending transactions. Conventional residential title work and commercial private lending present different risk profiles, and title companies experienced in one may not be well suited to the other.

How Geraci LLP Supports Private Lenders on Title Insurance Issues

The attorneys at Geraci LLP have spent years working with private lenders on exactly these issues. From negotiating endorsement packages on complex commercial transactions to advising on state-specific title insurance frameworks, the firm provides the practical guidance that lenders need to close transactions with confidence that their title coverage is complete.

When a title company refuses an endorsement, when a new lending state presents unfamiliar title insurance rules, or when a transaction requires creative solutions to fill coverage gaps, Geraci LLP has the experience to help.

To discuss title insurance endorsement strategies for your lending program, contact Geraci LLP at (949) 403-3488 or visit us at 90 Discovery, Irvine, CA 92618.